From Success to Significance: A Primer For Business Owners On Building A Lasting Legacy

A recent survey of business owners indicated that 75% of business owners would like to exit their business within the next 10 years. That means it is possible that 4.5 million privately held businesses will transition within the next 10 years representing nearly $14 trillion of business wealth at stake. Many business owners have worked years, if not a lifetime, to build their business. And the business represents by far the largest asset they own. So the stakes are high from an financial and emotional standpoint.

Unfortunately, many business owners may overlook crucial opportunities and face negative outcomes due to inadequate or nonexistent planning. The Exit Planning Institue estimates that, 58% of business owners do not have a written transition plan. As a result, these owners might miss the chance to create a lasting legacy, optimize wealth transfer to their heirs, preserve jobs for their employees, and continue supporting their local communities. The gap between the number of business owners seeking to transition and those who are actually prepared presents a significant gap.

Importance of Financial Planning

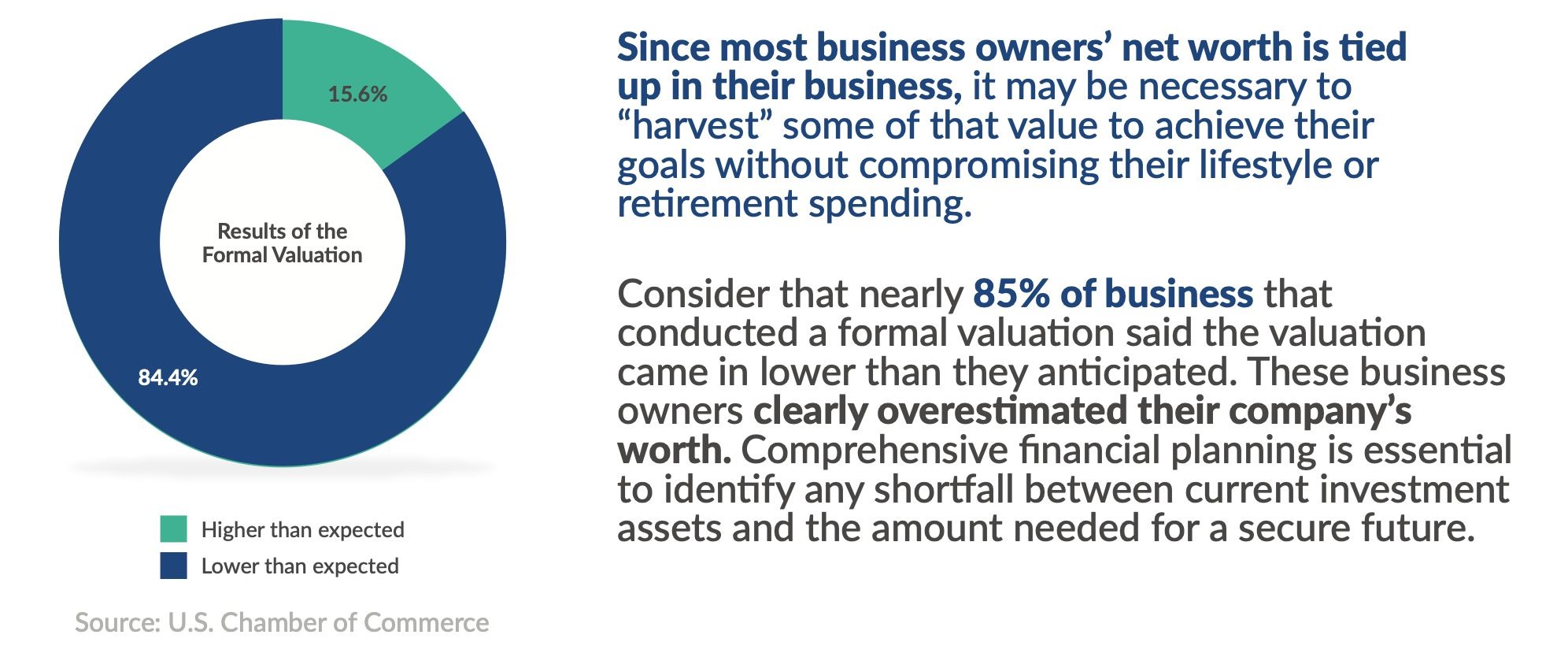

While assessing the current value of the business, owners should also work closely with their financial advisor on comprehensive financial planning. This process aims to determine if the owner's retirement and personal goals can be met with their existing investments, excluding the business equity.

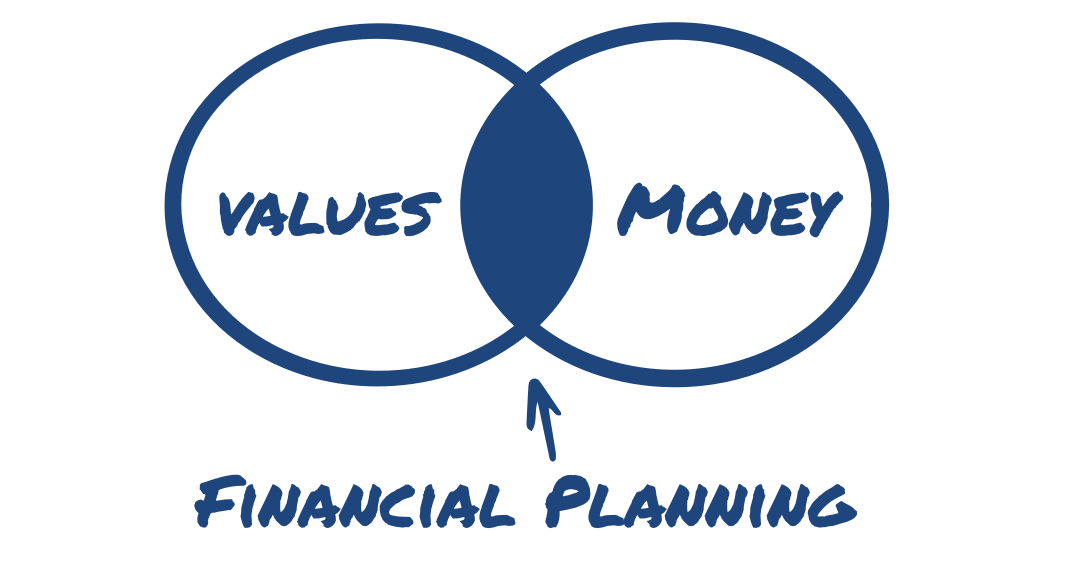

We recommend a values based approach to financial planning versus the traditional goals based approach. Values-based financial planning is an approach that not only considers an individual’s financial goals, but also incorporates their personal values, beliefs, and goals into the decision-making process. This approach recognizes that people may have different priorities when it comes to their values—something that other wealth management strategies, like goals-based financial planning, may not align with.

Although the goal is still growing your wealth, having financial strategies that align with what you believe, turns your financial plan from just a tool into a reflection of things you care about. It ensures that your financial resources will have the optimal impact on the people and causes you care about most.

A values based plan begins with identifying what matters most to you and includes your financial milestones, and benchmarking your current financial reality, including the current after-tax sales proceeds from the business. Your plan should illustrate the impact of selling at different points in time versus continuing to operate the business.

Important considerations include whether there will be enough assets after the sale to achieve your personal financial goals and whether there are additional assets that can be used for other purposes aligned with your objectives—for example, to make gifts to family members and charity (excess capital). Your plan should incorporate a Monte Carlo simulation, which utilizes thousands of different trials to give an overall probability of success of meeting the plan outcomes, taking various assumptions into account. Incorporating the potential volatility affords a more in-depth analysis of your ability to meet your financial goals and helps to inform a more thorough conversation to identify appropriate solutions.

The principal reason to engage in comprehensive values based financial planning early on is that it will require the business owner to think hard about what he or she wants to accomplish and how to balance competing priorities.

The principal reason to engage in comprehensive values based financial planning early on is that it will require the business owner to think hard about what he or she wants to accomplish and how to balance competing priorities.

Build Your Team

A good transaction team can identify potential problems and hash out solutions before it’s too late. It requires a team working together behind the scenes to ensure your hard work adds up to maximum gain. You can lose significant benefits without an integrated approach. The needed level of coordination cannot and does not happen on fragmented teams. In an ideal setting, each member of your support team is constantly asking each other questions. Your advisor knows you and your wealth-planning goals, and they can tap into the team’s greater resources to help you plan for a successful future with your well-deserved proceeds.

Some closely-held business owners may not have experience in selecting outside advisors suitable for their current situation. With the sale of the business, the business owner will need to expand the advisor team to obtain the best result. There may be a need to change advisors if existing ones aren’t up to the task. Some of the advisors most often required for the sale of a business include:

Certified Public Accountant (CPA)

The CPA is a key outside advisor to the closely-held business owner. The CPA typically has regular contact with the business and understands its structure and operations well. This individual can prove invaluable at every stage of the sale of a closely-held business, especially in making sure that the sale is accomplished in the most efficient manner from an income tax perspective.

Qualified appraiser

While the investment banker values the business for sale, gifts to family members, charity or irrevocable trusts require a “qualified appraiser” for tax purposes. Qualified appraisers may value the business for the purpose of making gifts, taking into account any valuation discounts that may be available on the transfer of a closely-held business interest under the Internal Revenue Code.1 By potentially discounting the value of the closely-held business, transfers of those business interests may result in estate, gift and GST tax savings.

Attorneys

Typically, a closely-held business owner will require a few attorneys with different areas of specialization:

1. A corporate/transactional attorney to structure and execute the transaction;

2. An income tax attorney who may assist in structuring the purchase agreement to minimize income tax liability for the seller, such as proper apportionment between capital gains and ordinary income tax liability; and

3. An estate planning attorney to create trusts and other related vehicles to mitigate transfer taxes (gift, estate and generation-skipping taxes) if the business owner’s overall estate tax dictates wealth planning to mitigate transfer taxes. Typically, estate planning is most tax effective when done well in advance of the corporate transaction. Unfortunately, more often than not, estate planning is an afterthought, and the estate planning attorney is brought in at the last minute before the sale closes. Significant tax planning opportunities are often lost in those situations.

Investment banker

Although a closely-held business owner has typically worked with accountants and attorneys in the past, it’s unlikely that she’s worked with an investment banker. Yet, for larger businesses, choosing the right investment banker can be critical to maximizing the sales price. Investment bankers specialize in the purchase and sale of businesses. Finding an investment banker who specializes in the business owner’s industry is necessary to help to determine a proper value and identify potential buyers. A business owner who doesn’t work with an investment banker (or selects one who lacks experience or expertise in the area) may end up getting less in a sale. While the help of investment bankers may not be available for small business owners, business brokers may be a viable alternative.Financial advisor

Business owners tend to invest most of their capital back into the business and, typically, don’t have large outside investment accounts. As such, they may not be sophisticated users of wealth management services. If the business owner wants to sell the business, this lack of understanding needs to change. A recent survey of business owners found that their most trusted advisor has shifted over the last decade. Today, business owners view their financial advisor as their most trusted advisor. Financial advisors usually know more about their financial picture and their values than any other advisors.

An experienced financial advisor can help with the pre-sale financial planning necessary to answer the pivotal question of whether the business owner will receive enough from the sale, after taxes, to support the owner’s and her family’s lifestyle. As part of the planning process, the financial advisor will create an asset allocation strategy for the sale proceeds and implement investments to carry out the financial and estate planning strategy to help achieve the family’s goals.

Think About Your Legacy

It’s nearly universal: business owners want their children to forge their own path in the world. They are not necessarily looking for their children to follow in their footsteps or take orders on how to manage the assets and opportunities they have been given.

Many business owners struggle with the fear of encouraging children to believe that the family’s wealth is an entitlement. Yet, they want to give their subsequent generations more freedom to forge their own path, unencumbered by financial considerations.

Most wealth builders acknowledge that other people played a role in their financial success. Among those who agreed others helped them, spouses get the top nod (acknowledged by 71% of wealth builders) and more than half say a financial advisor helped them on their way to financial success.

Yet, we often hear that many business owners are concerned that their children don’t know how to manage wealth of their own or maintain what might be given to them. There are fears that giving their children too much financially leads to a lack of motivation to build their own successful path in life. Legacy includes leaving money to family, but even more meaningful is the ability to pass down values and make an impact on others through philanthropic endeavors.

If sustainable multigenerational wealth transfer is among your goals, it is critical to focus not only on traditional financial, tax, and estate planning, but also on legacy planning. Legacy planning is what we call “the human side of planning”—planning that ensures that your family will stay strong and united for many generations. Just like financial planning, legacy planning is a process that begins during your lifetime and has a significant effect on the legacy you pass to your heirs. The better your lifetime planning, the more impactful and long-lasting your legacy will be for your heirs.

If you want your legacy to live on and your family to flourish after you are gone, you must make a commitment to build a solid legacy during your lifetime. In the absence of purposeful planning, the odds are against you. Legacy planning concentrates on the key elements of success: improving communication skills and trust within the family, educating and preparing your heirs to inherit all forms of capital, and defining your family’s unique purpose and mission, which is the superglue that will keep the family together for generations.

Steps to Take to Secure Your Legacy

Schedule regular family meetings to discuss the business of being a family, to grow family unity, and encourage individual development and education and ensure that each family member flourishes;

Identify family values to which every family member agrees;

Define a plan of family governance. Define the roles and responsibilities around family wealth and define a mechanism for decision-making and resolution of conflict that inevitably arise in every family;

Schedule regular family vacations and encourage everyone to attend. Consider ways to inspire and facilitate family meetings and vacations when you are gone;

Consider family philanthropy as a way to make a difference in the world, and increase effective communication, education, and family harmony.

Conclusion

In planning for a successful exit, the owner's readiness to sell is just as crucial as making the business appealing to potential buyers. If an owner hasn’t developed a solid plan for their next phase—whether it's an engaging retirement, pursuing hobbies or bucket-list goals, or exploring new entrepreneurial ventures—they may not be truly prepared to sell and could face disappointment post-transition. A survey conducted a year after the sale revealed that three out of four business owners “profoundly regretted” 1 the decision. This regret was not so much about missing their business but rather about not having sufficiently considered what their daily life would look like after leaving their office or factory.

Although it might initially seem like a minor issue, failing to develop a thoughtful personal plan for life after the business transition can significantly impact both the success of the sale and the owner's satisfaction with the outcome. Owners who haven't carefully planned their post-transition life are less likely to successfully complete the sale and are more prone to regret their decision if they do. By collaborating with family members, a trusted financial advisor, and experienced professionals who specialize in aligning personal and financial goals,

owners can better prepare themselves for a fulfilling transition to life after the sale.

1 Christopher Snider, “Walking to Destiny” 2nd edition